If you’ve ever wondered how surety bonds differ from traditional insurance, you’re not alone.

Many contractors hear the terms used together and assume they serve the same purpose. After all, both involve risk management, both require premiums, and both are often required before work can begin. However, that’s where the similarities largely end.

Surety bonds and insurance are designed to accomplish very different objectives. Understanding the distinction can help contractors stay compliant, qualify for larger projects, avoid costly delays, and position their businesses for long-term growth.

Whether you’re applying for a contractor license, bidding on a public works project, or simply trying to understand your insurance requirements, knowing the difference between a surety bond and an insurance policy is essential.

Why Surety Bonds Are Not Insurance

The biggest misconception about surety bonds is that they’re a type of insurance policy.

In reality, a surety bond functions more like a financial guarantee than an insurance product.

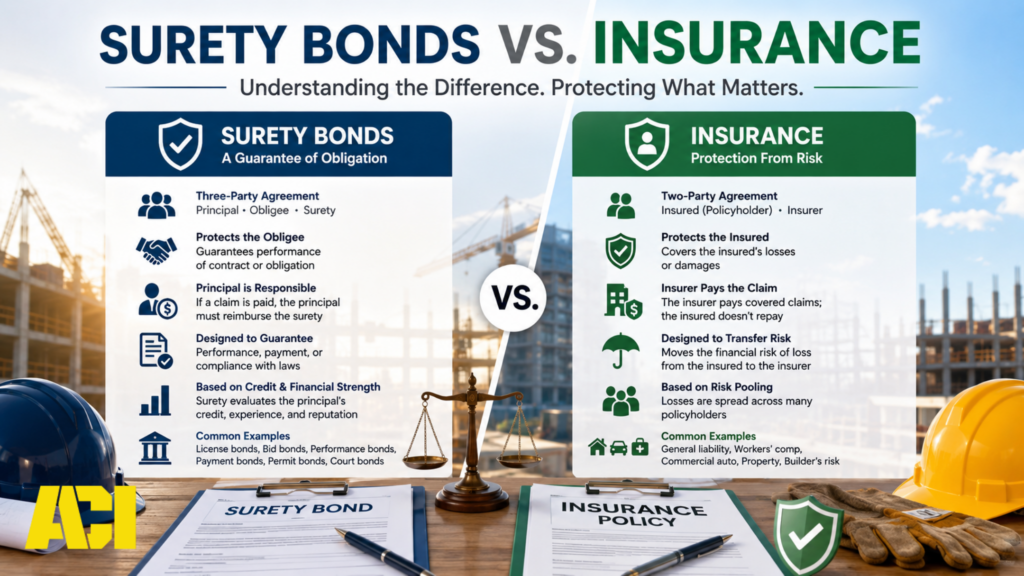

Insurance is designed to protect the policyholder from unexpected losses. A surety bond, on the other hand, guarantees that a contractor or business will fulfill a specific obligation, whether that’s complying with licensing requirements, completing a project according to contract terms, or paying subcontractors and suppliers.

The difference becomes clearer when you look at who is actually being protected.

When a contractor purchases a general liability policy, the insurance company is protecting the contractor from covered claims and losses. If a covered incident occurs, the insurer pays the claim according to the terms of the policy.

With a surety bond, the protection is provided to the party requiring the bond, not the contractor purchasing it. If the bonded contractor fails to meet their obligations, the surety company may compensate the harmed party. Unlike insurance, however, the contractor is typically responsible for reimbursing the surety for any valid claims paid.

This distinction is what makes bonds fundamentally different from insurance.

Understanding the Three-Party Relationship

One of the clearest differences between a surety bond and an insurance policy is the structure of the agreement itself.

Insurance is a two-party agreement involving the insured and the insurance company. The policyholder pays premiums, and the insurer agrees to assume certain risks in exchange.

A surety bond involves three parties:

- The Principal, which is the contractor or business obtaining the bond

- The Obligee, which is the project owner, government agency, or licensing authority requiring the bond

- The Surety, which is the company guaranteeing the Principal’s performance

This three-party relationship exists because the purpose of the bond is to provide assurance to the Obligee that the Principal will fulfill their obligations.

In many ways, a surety bond acts as a form of financial backing and credibility, demonstrating that the contractor has the resources, experience, and reliability necessary to complete the work as promised.

Who Is Actually Protected?

Another major distinction comes down to who receives the benefit of the protection.

A surety bond protects the Obligee. If the Principal fails to perform, violates regulations, or does not fulfill contractual obligations, the harmed party may have recourse through the bond.

Insurance protects the policyholder. If a covered loss occurs, such as property damage, bodily injury, or a lawsuit, the insurance policy helps protect the insured from the financial consequences.

This difference is why contractors often need both. The bond protects project owners and regulatory agencies, while insurance protects the contractor’s business.

How Risk Is Handled Differently

Insurance and surety bonds also differ significantly in how risk is evaluated and distributed.

Insurance companies operate on a risk-pooling model. Premiums collected from many policyholders are used to pay the claims of the relatively small number who experience covered losses. Insurance companies expect claims to occur and price their policies accordingly.

Surety companies take a different approach.

Because the contractor is ultimately responsible for reimbursing claims, the surety expects little to no loss. Before issuing a bond, the surety carefully evaluates the contractor’s financial strength, credit history, experience, and reputation.

This is why bonds are often viewed more as a form of credit than a traditional insurance product.

The stronger a contractor’s financial profile, the easier it typically is to obtain bonding and secure larger bond limits.

Why Project Owners Require Surety Bonds

One of the biggest reasons surety bonds exist is to reduce risk for project owners.

When a developer, municipality, school district, or government agency awards a contract, they are trusting a contractor to complete a project on time, within budget, and according to specifications. If the contractor fails to perform, the financial consequences can be significant.

A surety bond provides confidence that the project can move forward even if problems arise.

For example, if a contractor abandons a project midway through construction, a performance bond can help compensate the project owner for resulting damages or assist in arranging for project completion.

Without that protection, the owner could be forced to absorb substantial financial losses, delays, and legal expenses.

This added layer of security is why bonding requirements are common on public works projects and increasingly common on larger private developments.

Common Types of Surety Bonds for Contractors

Contractors may encounter several different bond requirements throughout their careers.

License and Permit Bonds

These bonds are often required by state and local licensing agencies before a contractor can legally operate. They help ensure compliance with applicable laws and regulations.

Bid Bonds

Bid bonds provide assurance that a contractor will honor their bid and enter into a contract if selected for the project.

Performance Bonds

Performance bonds guarantee that the contractor will complete the project according to the agreed-upon contract terms.

Payment Bonds

Payment bonds help ensure subcontractors, suppliers, and laborers receive payment for their work and materials.

Fidelity Bonds

Fidelity bonds protect businesses against losses resulting from employee dishonesty, theft, or fraudulent activities.

Each bond serves a unique purpose, but all are designed to provide assurance that obligations will be fulfilled.

Need Help With Surety Bonds or Contractor Insurance?

Whether you’re applying for a contractor license, bidding on a public project, or reviewing your current insurance program, understanding your bonding and insurance requirements is critical to protecting your business and winning more work.

At Affordable Contractors Insurance (ACI), we help contractors across the country secure the coverage and bonding solutions they need to stay compliant, meet contract requirements, and confidently pursue new opportunities.

Our team can help you:

- Evaluate your current insurance program

- Determine which bonds your business may need

- Review contract insurance requirements

- Identify coverage gaps before they become costly problems

- Find competitive options tailored to your trade and operations

Not sure if your next project requires a bond, insurance, or both?

How Bond Claims Work

Another area that often causes confusion is the claims process.

When an insurance claim is filed, the insurer investigates the loss and, if covered, pays the claim on behalf of the policyholder.

A surety bond claim works differently.

When a claim is filed against a bond, the surety investigates whether the Principal failed to fulfill the obligations outlined in the bond agreement. If the claim is determined to be valid, the surety may compensate the harmed party.

However, because the bond is a financial guarantee rather than risk transfer, the contractor is generally required to reimburse the surety for any money paid out.

This reimbursement obligation is one of the key differences between surety bonds and insurance.

It’s also why surety companies place such a strong emphasis on underwriting standards before issuing bonds.

Learn more about how surety bonds work from the Surety & Fidelity Association of America (SFAA)

Where Insurance Fits Into the Picture

While bonds help guarantee performance and compliance, insurance protects contractors from the financial consequences of accidents, injuries, property damage, and lawsuits.

Common insurance policies for contractors include:

- General Liability Insurance

- Workers’ Compensation Insurance

- Commercial Auto Insurance

- Builders Risk Insurance

- Professional Liability Insurance

- Umbrella Insurance

These policies help protect a contractor’s financial stability when unexpected events occur.

Unlike surety bonds, insurance policies are designed specifically to transfer financial risk from the contractor to the insurance company.

A Real-World Contractor Example

Imagine a general contractor wins a municipal building project.

Before work begins, the city requires the contractor to provide both a performance bond and proof of general liability insurance.

During construction, a visitor trips over equipment and suffers an injury. The resulting claim would typically fall under the contractor’s general liability insurance policy.

Now imagine the contractor experiences financial difficulties and walks away from the project before completion.

In that scenario, the performance bond may come into play to protect the city from the contractor’s failure to fulfill their contractual obligations.

The insurance policy and the bond address two entirely different risks, which is why project owners frequently require both.

Why Bonding Can Help Contractors Win More Work

Many contractors initially view bonding requirements as another hurdle to overcome.

In reality, bonding can become a significant competitive advantage.

Being bondable demonstrates financial strength, reliability, and professionalism. It signals to project owners that an independent third party has evaluated your business and determined that you have the capacity to fulfill your obligations.

As contractors grow and pursue larger commercial or public projects, bonding often becomes less of an option and more of a necessity.

In many cases, the ability to secure larger bond limits directly impacts the size and type of projects a contractor can pursue.

For contractors looking to expand their operations, strong bonding capacity can open doors to opportunities that would otherwise be unavailable.

Frequently Asked Questions About Surety Bonds and Insurance

Can a Surety Bond Replace Insurance?

No. Surety bonds and insurance serve different purposes and are not interchangeable. Most contractors need both to satisfy project requirements and protect their businesses.

Do Surety Bonds Protect the Contractor?

Not directly. Surety bonds primarily protect the project owner, licensing authority, or other party requiring the bond.

Why Are Bonds Commonly Required on Public Projects?

Public entities use bonds to protect taxpayer-funded projects from contractor default, non-performance, and unpaid subcontractors or suppliers.

Does Every Contractor Need a Bond?

Not necessarily. Requirements vary by state, trade classification, license type, and project size. Some contractors may only need a license bond, while others may require bid, performance, and payment bonds for specific projects.

The Bottom Line

Although surety bonds and insurance are often discussed together, they serve fundamentally different functions.

Insurance protects contractors from covered losses and claims. Surety bonds provide a financial guarantee that contractors will fulfill contractual, legal, or regulatory obligations.

Insurance is designed to transfer risk. Surety bonds are designed to guarantee performance and compliance.

Understanding the difference can help contractors make informed decisions, maintain compliance, qualify for larger opportunities, and avoid unnecessary headaches when projects are on the line.

If you’re unsure whether your business needs a bond, an insurance policy, or both, speaking with a contractor-focused insurance advisor can help ensure you’re properly protected before your next project begins.