Imagine you just found a car insurance policy that offers great, affordable contractors coverage for a fraction of what you’re currently paying. It’s possible to secure affordable coverage without sacrificing protection but many people overlook key strategies.

With Affordable Contractors Insurance, it’s possible to get the protection you need without compromising on quality or key coverages.

Let’s walk through how you can build a policy that aligns with your specific needs—and your financial goals.

Understanding Full Coverage Contractors Insurance

What “Full Coverage” Means

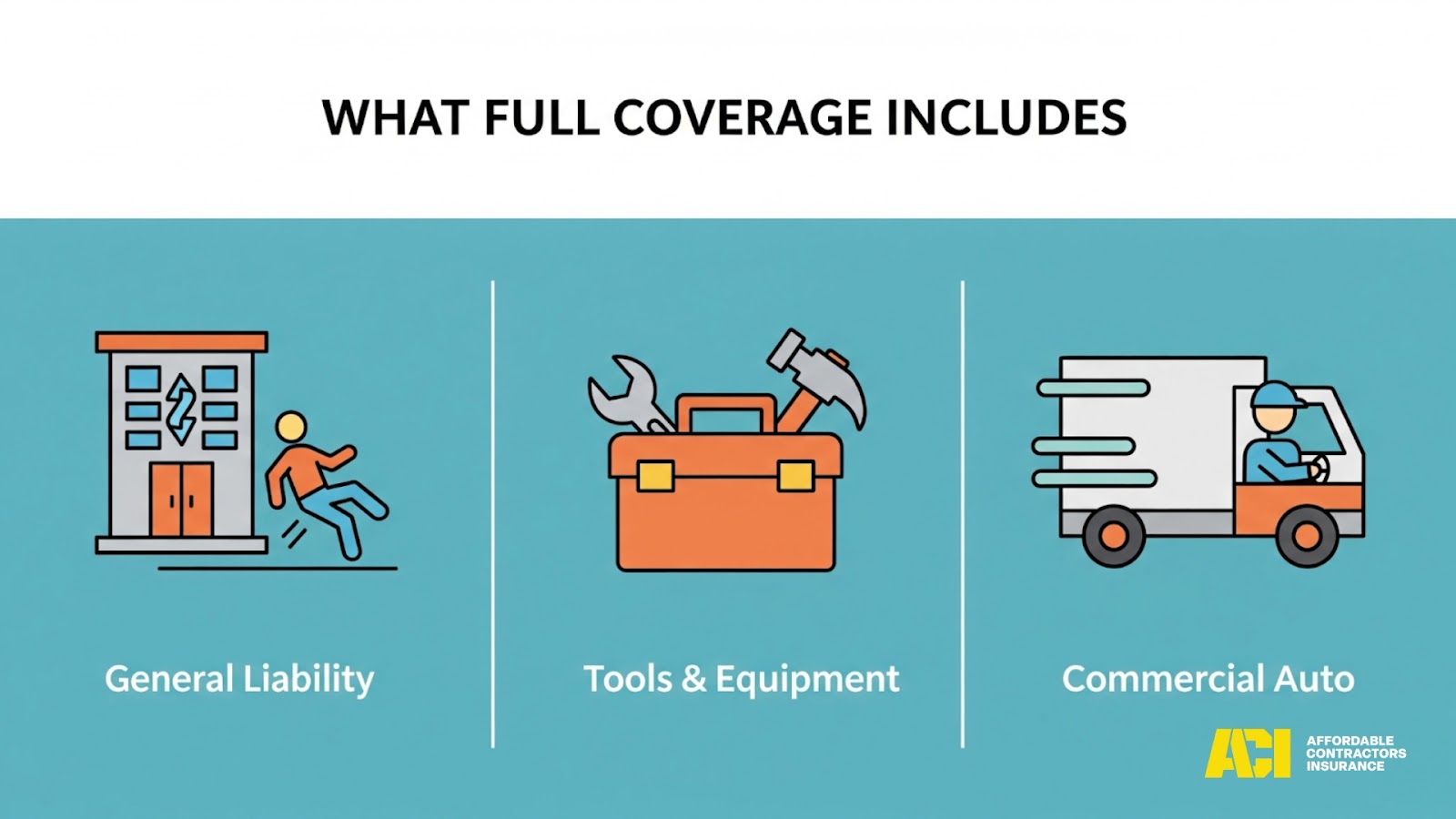

Full coverage for contractors generally includes three essential protections:

- General Liability for third-party injury or damage

- Tools & Equipment coverage for theft or damage

- Commercial Auto insurance for vehicles used on the job

Together, these coverages form a solid foundation to keep your business operating smoothly in the face of accidents or unexpected challenges.

Why Liability Matters

Each project presents risks, but general liability coverage helps ensure you’re not left vulnerable to legal or financial consequences.

Affordable Contractors Insurance provides tailored protection designed to meet the demands of your work environments.

Protecting Your Tools on the Job

Your tools are essential assets. Equipment coverage through Affordable Contractors Insurance helps you stay productive if your gear is lost, stolen, or damaged.

Key Protections to Include in Your Policy

Uninsured/Underinsured Coverage

Working with subcontractors or vendors who carry minimal insurance? Uninsured and underinsured coverage adds another layer of security to protect your business.

Personal Injury Protection (PIP)

PIP covers medical-related expenses resulting from accidents involving you or your team. This protection ensures your business stays resilient during difficult times.

Comparing Quotes: The First Step to Potential Savings

Why Quotes Matter

Comparing quotes is a smart way to ensure your insurance aligns with your current needs and possible budget expectations.

Affordable Contractors Insurance helps you assess coverage features side by side—so you’re confident in what you’re choosing.

How Affordable Contractors Insurance Supports You

We make it easy to compare policies with the same limits and deductible structures. That means clarity and transparency from the start.

Local Expertise with Wide Reach

Affordable Contractors Insurance brings together national expertise and local market knowledge to help you access customized coverage with potential advantages.

Exploring Discounts for Affordable Coverage

Multi-Policy Options

By combining multiple policies under one provider, you may potentially access additional perks and possible efficiencies.

We offer bundled options to simplify your coverage and support broader protection strategies.

Safety Incentives

Using modern safety practices and site monitoring can help you qualify for possible premium incentives with Affordable Contractors Insurance.

Claims-Free Recognition

If your business has a strong record of safe operation, you may be eligible for loyalty rewards or specialized policy adjustments.

The Impact of Deductibles on Your Premiums

How Deductibles Affect Coverage Flexibility

- Adjustable Options: Choose from different deductible levels that align with your business’s risk tolerance.

- Preparedness: Select a deductible that balances your confidence in financial preparedness with your desired protection.

- Custom Structuring: Our team can help structure your policy with a deductible option that meets your operating needs.

Tailoring Coverage to Your Project Needs

Every contractor has a unique business model. That’s why we recommend customizing your coverage to suit your operations.

Short-Term Projects benefit from flexible coverage durations.

Specialty Equipment may require expanded protections.

Routine, low-risk work can allow for modified policy terms.

Affordable Contractors Insurance adapts your policy to reflect your working reality—not a one-size-fits-all plan.

High-Risk Projects: Options for Affordable Contractors Coverage

Specialized Policy Support

High-risk work doesn’t mean you have to accept less favorable terms. Affordable Contractors Insurance helps connect you to policies designed for specialized trades.

Safety Course Credits

If your team has completed safety or compliance training, you may qualify for possible enhancements to your coverage package.

Non-Standard Risk Solutions

We understand niche needs and can provide thoughtful, competitive options even for contractors with unique risk profiles.

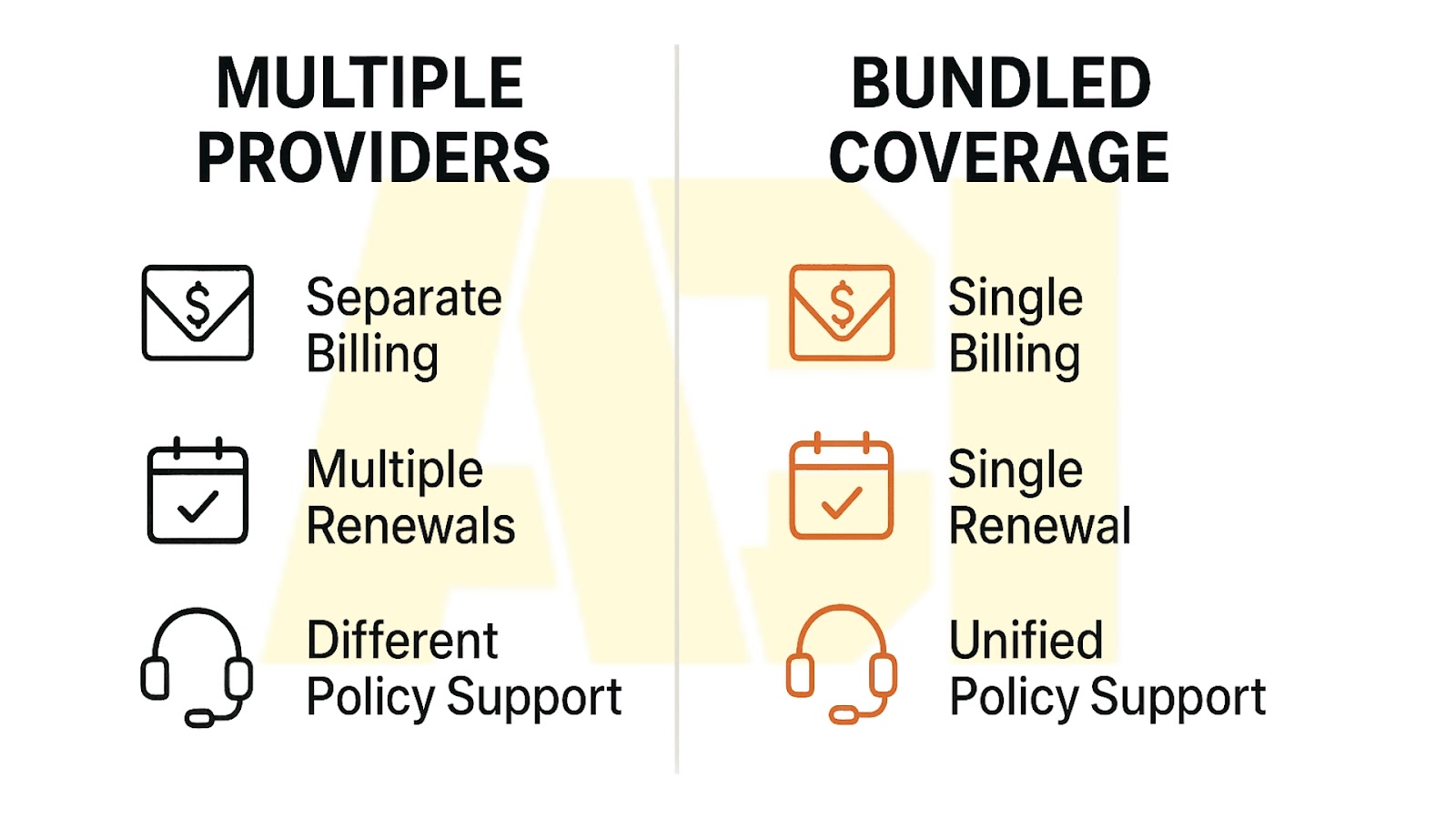

The Benefits of Bundling Policies

Convenience & Coverage in One Place

Managing multiple policies across your business? With Affordable Contractors Insurance, bundling can simplify your paperwork and service process.

Fewer Renewals, Fewer Headaches

Unified billing and policy timelines mean fewer administrative tasks and more time for your worksite responsibilities.

The Role of Business Credit in Insurance Rates

Why Business Credit Matters

A strong business credit history signals responsibility and stability, which insurers consider when assessing risk.

Affordable Contractors Insurance uses this data to help structure your policy in a way that reflects your strengths.

Improve and Monitor for Added Confidence

Staying on top of your credit report may support more favorable terms as your business grows.

Maintaining a Clean Claims Record

How Safety Translates to Opportunity

Contractors with a history of safe operations are often viewed as lower-risk.

This recognition can lead to policy benefits such as increased flexibility and possible eligibility for rewards or perks.

Keeping It Clean

Implement safety training, routine audits, and documentation protocols to support a strong safety record—and safeguard your ability to qualify for enhanced coverage terms.

Regular Policy Reviews: A Smart Strategy

Why Annual Reviews Are Crucial

Staying current with your policy ensures it grows with your business.

Affordable Contractors Insurance encourages annual check-ins to ensure your coverage keeps pace with your needs and potential opportunities for updates.

Adapting as You Grow

A new project, new equipment, or staff changes might mean you’re due for a quick policy adjustment. Let’s make sure you’re still protected—appropriately and efficiently.

Negotiating with Your Provider

Partnering for Better Results

At Affordable Contractors Insurance, we welcome policy discussions.

Bring any updated business information, inquire about newly available discounts, or request an adjustment in your deductible or terms.

Our team is committed to helping you maximize your plan’s value.

Common Misconceptions About Full Coverage

| Myth | Reality |

| Full coverage covers everything | Full coverage includes liability, equipment, and vehicle protections—not every possible situation |

| Older tools don’t need insurance | If your tools are crucial to your operations, they still need protection |

| The lowest price means full coverage | It’s more important to ensure your coverage matches your actual risks and needs |

Final Tips for Securing Affordable Protection

- Compare Quotes Regularly – Policy options change, and potential new benefits may emerge.

- Adjust Your Deductible – Reassess your business’s financial cushion and risk comfort.

- Bundle Thoughtfully – Consolidate policies for fewer admin hassles and possible added protection.

- Emphasize Safety – Create long-term advantages through responsible operations and clean claims history.

Conclusion: Build Smarter Protection with Confidence

Securing affordable coverage doesn’t mean cutting corners on protection. It means making informed decisions—evaluating your risks, customizing your policy, and partnering with a provider who understands your business.

With Affordable Contractors Insurance, you gain access to flexible, reliable coverage built around your unique needs—from general liability to equipment, commercial auto, and more.

Whether you’re adjusting deductibles, reviewing policies annually, or exploring bundling options, you’re taking proactive steps toward protecting your business without compromising quality.

Your next project deserves the right protection.

Let Affordable Contractors Insurance help you build a smarter, stronger insurance plan that works for you—today and into the future.

👉 Get a FREE quote from Affordable Contractors Insurance today and explore how smart, customized coverage can keep your business safe—without compromise.

Frequently Asked Questions

Q: What types of coverage are included in full contractors’ insurance?

A: Full contractors’ insurance typically includes general liability, tools and equipment coverage, and commercial auto insurance. These cover core risks faced by contractors on job sites and in daily operations.

Q: Is it possible to get affordable coverage without sacrificing protection?

A: Yes. With Affordable Contractors Insurance, you can tailor a policy to match your business’s specific needs—ensuring you get essential coverage with potential savings through smart structuring and review.

Q: How can I lower my insurance premium without reducing important coverage?

A: Consider increasing your deductible, bundling multiple policies, maintaining a clean claims record, or completing safety training. Affordable Contractors Insurance evaluates each factor to help you find possible efficiencies.

Q: What does uninsured or underinsured coverage mean for contractors?

A: This coverage protects you when subcontractors, clients, or third parties involved in a claim do not carry adequate insurance. It helps fill the gap to keep your business financially protected.

Q: Can high-risk contractors still get affordable insurance?

A: Yes. Affordable Contractors Insurance works with contractors in higher-risk trades by offering specialized policy structures, safety-based incentives, and flexible underwriting options.

Q: Why should I review my contractors’ insurance policy annually?

A: Business needs evolve—new projects, tools, or team changes could require policy updates. Regular reviews with Affordable Contractors Insurance ensure your coverage remains aligned with your current risk exposure.

Q: What is “General Liability Only” insurance?

A: It’s a streamlined form of coverage that protects against third-party injury or property damage claims. However, it does not cover your equipment, vehicles, or employee-related medical needs.

Q: Does my credit score affect my contractors’ insurance rate?

A: Yes. A strong business credit score may support more favorable terms. Affordable Contractors Insurance considers financial responsibility when tailoring your policy.

Q: How does bundling insurance policies help contractors?

A: Bundling allows you to combine coverages—like general liability and commercial auto—under one provider. This can simplify management and unlock possible administrative or service-based advantages.

Q: Where can I get a personalized contractors’ insurance quote?

A: Visit Affordable Contractors Insurance and request a free, no-obligation quote. You’ll receive expert guidance tailored to your trade, location, and coverage goals.