Think of your contracting business as a house: without a solid foundation, it risks collapsing under pressure. Just as a sturdy frame supports your structure, the right insurance coverage from Affordable Contractors Insurance (ACI) protects your contracting business from potential liabilities, enhances your reputation, and helps grow your contracting business with the right insurance. Many contractors overlook this crucial aspect, but it could be the key to unlocking larger contracts and sustainable growth.

Why Contractor Insurance Is Crucial for Business Growth

When you’re running a contracting business, contractor insurance isn’t just optional—it’s essential. ACI Insurance offers solutions that help safeguard your company against costly lawsuits and claims.

Protect Your Business With Confidence

Accidents happen. Whether it’s property damage or an injured worker, a single incident can put your business in jeopardy. ACI’s contractor insurance protects against:

- Legal defense costs

- Employee injury claims

- Client disputes and lawsuits

With ACI, you get more than a policy—you gain trust, credibility, and peace of mind.

Explore ACI’s Contractor Insurance Plans

👉Get a quote from Affordable Contractors Insurance and see how much you can save.

Understanding the Importance of Contractor Insurance

When you’re running a contracting business, understanding the importance of insurance coverage is crucial for your success. Contractor insurance isn’t just a checkbox; it’s your safety net against potential liabilities. Accidental property damage or injuries can turn a single incident into a financial nightmare, jeopardizing everything you’ve built.

With the right coverage, you not only protect your contracting business but also gain financial security—covering legal defense costs and claims from client or employee injuries and mistakes.

Moreover, many clients require proof of insurance before hiring, so having comprehensive contractor insurance helps build trust and credibility. The costs can vary, influenced by your trade, business size, and location, but the peace of mind it provides is invaluable.

Key Types of Insurance Coverage for Contractors

Choosing the right insurance products is essential to protect your business from multiple risk angles. ACI offers a range of tailored coverages for contractors, including:

General Liability Insurance

Covers third-party bodily injury, property damage, and legal defense. Many contracts require proof of this before work even begins.

Workers’ Compensation Insurance

Required in most states, this coverage ensures injured workers receive wage replacement and medical benefits—while protecting your business from lawsuits.

Tools & Equipment Insurance

Don’t let theft or damage slow you down. ACI covers your essential gear so you can get back to work—fast. Whether it’s stolen tools, damaged equipment, or lost productivity, our coverage ensures your business stays on schedule and on budget.

Professional Liability Insurance

Also known as errors & omissions, this coverage protects you against claims related to negligence, missed deadlines, or substandard work that results in financial loss for your clients. It’s essential for maintaining credibility and avoiding costly legal battles—especially in complex or high-stakes projects.

Assessing Your Insurance Needs as a Contractor

To effectively assess your insurance needs as a contractor, it’s essential to identify the specific risks your business faces, such as property damage, employee injuries, and equipment theft.

Start by gathering relevant business information, like your annual revenue, number of employees, and types of projects you undertake. This data helps determine the appropriate coverage options tailored to your needs.

ACI helps you evaluate your needs based on:

- Annual revenue

- Project size and scope

- Number of employees

- State and local licensing requirements

- Client insurance mandates

Consider the value of your tools and equipment when selecting coverage to ensure you’re adequately protected against loss or damage.

Regularly evaluating your insurance needs is key as your business evolves; adjusting coverage helps you avoid over-insurance or gaps that could leave you vulnerable.

Steps to Obtain Contractor Insurance with ACI

Getting insured with ACI is simple and hassle-free. Here’s how to secure the right coverage for your business:

- Assess Your Needs

Identify your business risks and the types of coverage required for your trade, whether it’s general liability, workers’ comp, or tools and equipment coverage. - Gather Key Information

Have your business details ready—like annual revenue, employee count, and trade-specific information—to get accurate and competitive quotes. - Request a Free Quote

Use ACI’s fast online tool or speak directly with an agent to explore your options. - Review and Compare Coverage Options

ACI tailors your insurance options to match your trade and business size. Compare them to ensure you’re choosing the right fit in terms of limits, deductibles, and coverage types. - Select and Finalize Your Policy

Choose the policy that meets your legal and client requirements, then purchase it to activate your coverage. - Download Your COI Instantly

Once insured, you can immediately download your Certificate of Insurance (COI) to show proof of coverage to clients and meet contractual needs, and that your contracting business is protected!

Comparing Insurance Providers and Quotes

How do you choose the right insurance provider for your contracting business? Start by gathering 3-5 quotes from different insurance providers, ensuring they include similar coverage types, limits, and deductibles. This lays the groundwork for a fair comparison tailored to your specific needs.

Utilize online platforms for convenience or consult local agencies for a more personalized touch.

Once you have your quotes, carefully analyze the policy details. Look out for exclusions, coverage for completed operations, and the provider’s customer service reputation. These elements are crucial for comprehensive protection.

Also, consider how easily you can obtain Certificates of Insurance (COIs) from each provider, as this can impact your ability to secure contracts.

Choosing the Right Policy and Provider for Your Contracting Business

Selecting the right insurance policy is more than just a business requirement—it’s a smart investment in your company’s stability, reputation, and future growth. Here’s how to make the best choice and why ACI stands out as your ideal partner:

1. Assess Your Business Risks

Start by identifying the specific risks your contracting business faces. From job site injuries to property damage, ensure your policy—especially general liability insurance—covers these common exposures.

2. Make General Liability Your Foundation

General liability insurance is the essential first step. It covers third-party property damage, legal costs, and client requirements—all in one affordable, flexible package.

3. Protect Your Team with Workers’ Comp

Meeting state requirements while protecting your employees is critical. ACI makes workers’ comp simple to set up and manage.

Coverage Includes:

- Medical expenses

- Lost wages

- Legal liability

- Rehabilitation services

4. Consider Specialized Coverage Options

Some contracting work demands more than basic policies. ACI offers industry-specific add-ons such as:

- Builders Risk Insurance

- Pollution Liability

- Employment Practices Liability

- Umbrella Liability Insurance

5. Bundle to Save

You can reduce your premiums by bundling policies like general liability and commercial property insurance—saving up to 10–25%. Increasing deductibles and maintaining a clean claims history also helps lower costs.

6. Compare Providers: Why ACI is Different

When evaluating insurers, ACI stands out for its:

- Competitive pricing

- Transparent terms with no hidden fees

- Customizable coverage

- Fast, reliable claims processing

- U.S.-based support from contractor insurance experts

7. Review Coverage Regularly

As your business evolves, so should your insurance. Conduct annual reviews and adjust policies for new projects, larger teams, or expanded services.

8. Consult with Experts

Don’t go it alone. ACI’s licensed agents specialize in contractor insurance and are ready to help you build a policy tailored to your trade, size, and goals.

Managing Risks With Comprehensive Coverage

While your contracting business thrives on delivering quality work, managing risks effectively is just as crucial to your success. Comprehensive coverage, including general liability and workers’ compensation, helps protect your business from financial burdens related to accidents and injuries on the job site.

By implementing safety programs, you not only create a safer work environment but can also significantly lower your insurance premiums—by up to 25%! Regularly assessing your coverage ensures it evolves with your business needs, helping you avoid unnecessary costs.

Don’t forget about tools and equipment insurance, which safeguards your valuable gear against theft or damage, ensuring project timelines remain intact. Engaging with an experienced insurance agency can simplify navigating complex coverage options, ensuring you meet legal obligations and client requirements.

Embrace effective risk management to secure your business’s future and reinforce your reputation in the contracting community.

The Role of General Liability Insurance

General Liability Insurance acts as a safety net for contractors, shielding you from third-party claims related to bodily injury and property damage. This coverage is essential for maintaining financial stability and ensuring your business can thrive.

Here are four key benefits of having general liability insurance:

1. Protection from Claims: It covers legal fees and compensation costs for claims that arise on job sites.

2. Client Requirement: Many clients require proof of this insurance before awarding contracts, making it crucial for winning projects.

3. Completed Operations Coverage: It extends protection against claims that emerge post-project due to defects or negligence.

4. Affordable Investment: The average cost ranges from $75 to over $1,000 monthly, tailored to your trade and location, positioning it as a vital investment in your business’s future.

Protecting Your Employees With Workers’ Compensation

Every contractor knows that protecting your employees isn’t just a legal obligation but a crucial aspect of running a successful business. Workers’ compensation insurance is mandatory in most states, covering medical expenses and lost wages resulting from work-related injuries.

By investing in this coverage, you’re not only safeguarding your team but also shielding your business from potential lawsuits.

Implementing a robust safety program can also lead to discounts on premiums, demonstrating your commitment to protecting your employees.

Don’t forget, timely reporting of any injuries ensures prompt benefits, maintaining morale and minimizing downtime.

Specialized Coverage Options for Contractors

To effectively safeguard your contracting business, it’s essential to explore specialized coverage options tailored to your unique needs. These options can provide peace of mind and protect your hard work:

1. Builders Risk Insurance: This covers structures and materials during construction, shielding you against risks like fire or theft.

2. Pollution/Environmental Coverage: If your projects might produce contaminants, this protects you from environmental damage claims.

3. Umbrella Insurance: This extends liability coverage beyond your existing policies, offering extra protection for larger claims.

4. Employment Practices Insurance: With rising lawsuits related to employee misconduct, this coverage protects against claims like discrimination or wrongful termination.

Tips for Saving Money on Contractor Insurance

While navigating the complexities of contractor insurance, you can find several strategies to save money without sacrificing essential coverage. Implementing comprehensive safety programs can significantly reduce overall business risks, leading to potential savings on premiums.

Keep a strong claims history by minimizing claims, which can help you qualify for reduced premium rates. Consider increasing your deductibles; this often lowers your monthly payments while managing risk effectively.

Regularly evaluate and adjust your coverage needs to avoid over-insuring, ensuring you only pay for what you need. Don’t overlook discounts from insurers for proactive risk management practices like safety training or joining professional associations.

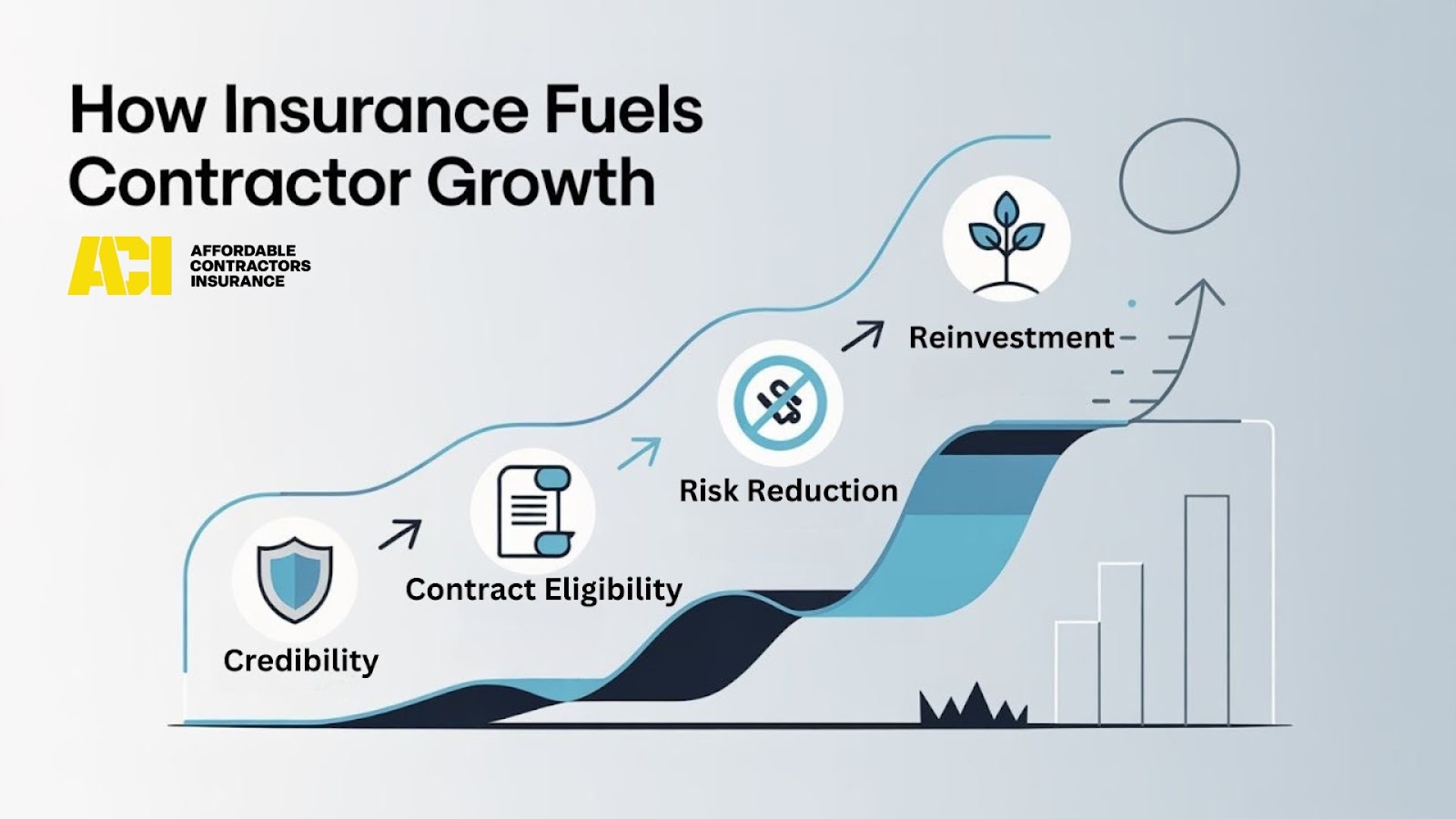

Insurance as a Growth Strategy

Insurance isn’t just protection—it’s a catalyst for business growth. The right coverage builds credibility, unlocks new opportunities, and helps you scale with confidence.

How Insurance Fuels Your Business Expansion

- Enhanced Credibility

General liability and other core policies show clients you’re professional and reliable—helping you win larger contracts and long-term partnerships. - Access to Bigger Projects

Many clients and government agencies require proof of insurance before awarding contracts. Having comprehensive coverage positions your business for more lucrative jobs. - Risk Mitigation

With the right protection in place, you can focus on growth without the fear of financial setbacks from lawsuits, property damage, or workplace injuries. - Operational Continuity

Insurance reduces downtime by covering legal fees, medical expenses, and business disruptions—keeping your projects on track. - Reinvest in Growth

A clean claims history and smart policy bundling can reduce your premiums, freeing up capital to reinvest in marketing, equipment, and hiring.

Why Growing Businesses Choose ACI

At ACI, we do more than insure—we empower contractors to grow.

✅ Get approved for bigger contracts

✅ Build client trust

✅ Reduce financial risk

✅ Reinvest savings from reduced premiums

Regularly Reviewing Your Insurance Policies

Regularly reviewing your insurance policies is essential for ensuring your coverage remains aligned with your contracting business’s evolving needs.

As your operations expand or you invest in new equipment, your risk exposure changes. By conducting an annual assessment, you can identify unnecessary coverage that might be costing you more than it’s worth, all the while ensuring the protection of your contracting business.

Staying informed about industry trends and legal requirements during your review helps ensure compliance and shields your business from potential liabilities.

Engaging with a certified insurance agent can offer tailored insights, so you can optimize your coverage and manage costs effectively.

Understanding Legal Requirements to Ensure Protection for Contractors

As you reassess your insurance coverage, it’s equally important to grasp the legal requirements specific to contractors. Understanding these helps you stay compliant and secure business opportunities.

U.S. Small Business Administration (SBA)

Here are four key points to consider:

1. General Liability Policy: Many clients require proof of this insurance to protect against claims of bodily injury and property damage, making it essential for compliance and trust.

2. Workers Compensation Insurance: If you have employees, most states mandate this coverage for work-related injuries and illnesses, ensuring both legal compliance and employee protection.

3. Contractor License: Some regions impose specific licensing and insurance requirements, such as Contractor License Bonds, to safeguard clients from financial loss.

4. Compliance Obligations: Staying updated on local laws and industry-specific regulations is crucial for maintaining the necessary coverage and fulfilling your obligations as a contractor.

Fulfilling these requirements can significantly enhance your reputation and help your business thrive.

Building Trust With Clients Through Proper Coverage

Building trust with clients hinges on your ability to demonstrate reliability, and proper insurance coverage plays a vital role in that equation. When you secure general liability and commercial insurance, you’re not just meeting legal requirements; you’re showing clients that you take their concerns seriously.

Comprehensive insurance coverage protects against financial liabilities from accidents or damages, reassuring clients that they’re in good hands. Clients often seek proof of proper coverage before hiring, and having it can set you, and your business, apart from the competition.

This commitment to risk management demonstrates professionalism and boosts your reputation, leading to repeat business and valuable referrals. By regularly updating your policies, you maintain that trust with clients, showcasing your dedication to their safety and security.

In this way, proper insurance isn’t just a requirement—it’s a cornerstone of lasting partnerships that can propel and protect your contracting business moving forward.

Conclusion

In the competitive world of contracting, the right insurance isn’t just a safety net—it’s your ladder to success. As you navigate projects and clients, remember that each policy you choose can either bolster your reputation or leave you vulnerable.

What happens if a client questions your credibility? Or if an unexpected incident occurs? By staying proactive and ensuring you have the right coverage, you’re not just protecting your business; you’re setting the stage for future growth and opportunity.

Frequently Asked Questions

Q: Why is contractor insurance important for business growth?

A: Contractor insurance provides a foundation of protection for your contracting business. It shields you from financial losses due to lawsuits, property damage, or employee injuries. Having insurance also boosts credibility, making clients more likely to trust and hire you—especially for larger contracts.

Q: What types of contractor insurance should I consider?

A: Key insurance types include:

- General Liability Insurance – Covers third-party bodily injury and property damage.

- Workers’ Compensation – Required in most states to cover employee injuries.

- Tools & Equipment Insurance – Protects your gear from theft or damage.

- Professional Liability (E&O) – Covers claims related to negligence or errors.

- Builders Risk, Pollution Liability, Umbrella Insurance, and others may apply depending on your trade.

Q: How do I assess which insurance coverage I need?

A: Start by evaluating:

- Your annual revenue

- Number of employees

- Size and scope of projects

- State/local licensing requirements

- Client insurance mandates

ACI helps tailor your coverage based on these details to avoid under- or over-insuring.

Q: How can I get a contractor insurance policy with ACI?

A: Follow these simple steps:

- Assess your business risks

- Gather key business information

- Request a free quote from ACI

- Compare coverage options

- Finalize and purchase your policy

- Instantly download your Certificate of Insurance (COI)

Q: How do I compare insurance providers effectively?

A: Evaluate:

- Premium costs

- Policy exclusions

- Completed operations coverage

- COI availability

- Customer service reputation

ACI stands out with transparent pricing, flexible policies, and fast claims support.

Q: What makes ACI a good choice for contractor insurance?

A: ACI offers:

- Competitive rates

- No hidden fees

- Industry-specific coverage

- Fast claims processing

- U.S.-based support from contractor insurance experts

Q: Can bundling insurance policies save me money?

A: Yes. Bundling policies like general liability and commercial property can potentially reduce premiums by 10–25%. Keeping a clean claims history and opting for higher deductibles may also help cut costs.

Q: How often should I review my insurance policy?

A: At least once a year—or sooner if your business grows, you hire more employees, or take on new types of work. Regular reviews help ensure your coverage stays aligned with your current needs.

Q: What are the legal insurance requirements for contractors?

A: Most states require:

- General Liability Insurance

- Workers’ Compensation Insurance (if you have employees)

Other requirements may vary based on your location and type of projects, so always check with local authorities or a licensed agent.

Q: How does insurance help me win more contracts?

A: Proof of insurance shows professionalism and compliance with legal and client requirements. Many clients (especially commercial or government) won’t award a contract unless you carry proper insurance, making coverage a powerful business development tool.

Q: What strategies can help lower my insurance premiums?

A:

- Implement safety programs

- Increase your deductibles

- Maintain a clean claims history

- Review your policy annually

- Bundle multiple policies

- Ask about risk management discounts

Q: Why is general liability insurance considered the foundation?

A: It covers third-party claims, legal fees, and property damage—all common risks on job sites. Without it, a single accident could jeopardize your entire business.

Q: How does workers’ compensation insurance protect my business?

A: It covers employees’ medical bills and lost wages from work-related injuries, shielding your business from lawsuits and ensuring you meet legal obligations.

Q: What’s the role of specialized coverage options?

A: They protect your contracting business beyond standard policies, including:

- Builders Risk Insurance – Covers in-progress construction

- Pollution Liability – For environmental risks

- Umbrella Insurance – For high-limit claims

- Employment Practices Liability – Protects against workplace-related lawsuits

Q: How does insurance support long-term business growth?

A: With proper coverage:

- You reduce financial risk

- Secure higher-value contracts

- Build trust with clients

- Protect against disruptions

- Free up funds to reinvest in equipment, hiring, and marketing